US FHFA Studying Bitcoin Acceptance in Housing Mortgage Lending

Key Takeaways

- FHFA is studying the use of cryptocurrency, particularly Bitcoin, in mortgage qualification assessments

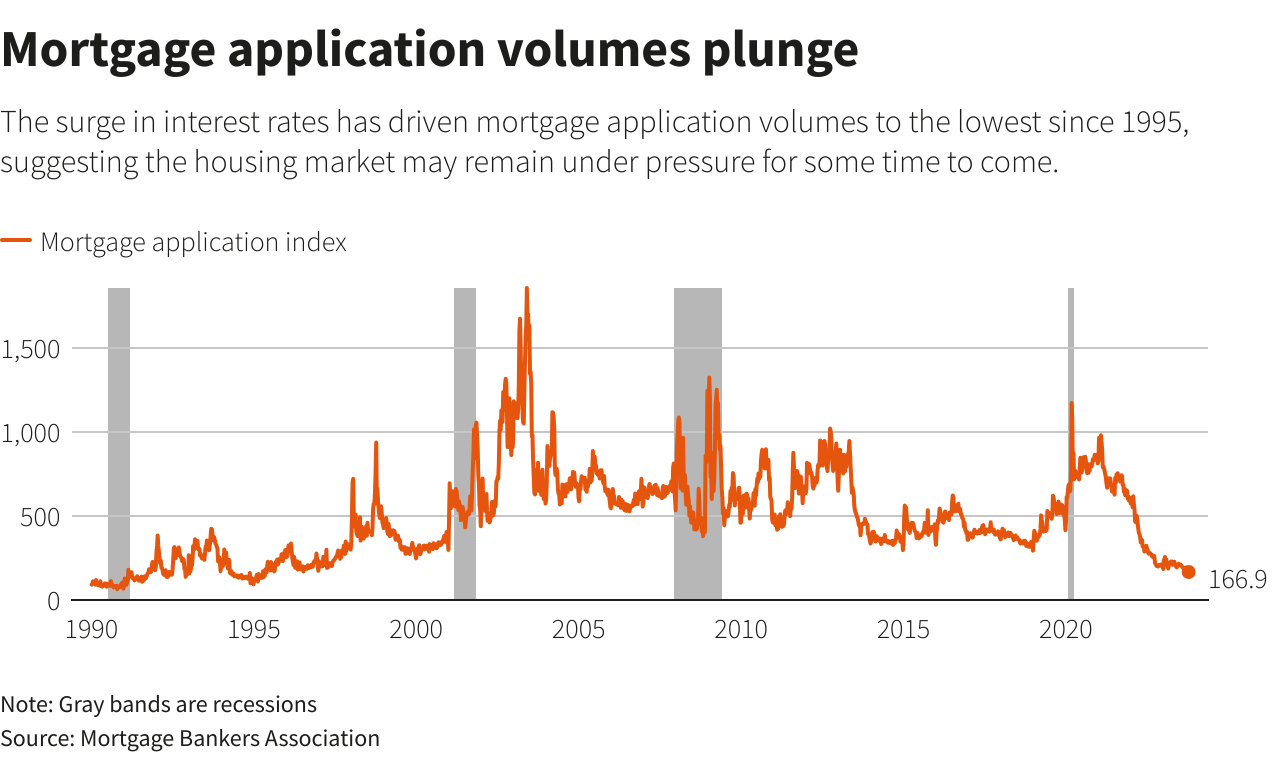

- The US housing market is struggling with mortgage applications declining sharply in recent years

- 20% of Americans own cryptocurrency (approximately 65 million people), creating significant market potential

- Risks remain due to Bitcoin’s high volatility and challenges in risk assessment

FHFA Opens Door for Cryptocurrency in Mortgages

The Federal Housing Finance Agency (FHFA) is taking significant steps toward integrating cryptocurrency into the mortgage lending system. Bill Pulte, head of FHFA, announced that the agency would “study the use of cryptocurrency holdings related to mortgage qualification.”

This move comes as the United States faces a severe housing crisis, with mortgage applications dropping to record lows.

Current State of the US Housing Market

Stable Homeownership but Declining Applications

While homeownership rates in the US have remained stable at 62% of the population over the past 50 years, the number of new mortgage applications has decreased significantly in recent years.

Causes of the Crisis

Supply Shortage:

- Construction pace has slowed down

- Many homes are purchased by investors rather than owner-occupants

- Elderly residents are not moving to senior housing facilities

Rising Borrowing Costs:

- Federal Reserve raised interest rates to combat inflation

- Making borrowing more expensive

Potential and Challenges of Bitcoin in Mortgages

The FHFA’s official recognition of cryptocurrency could open federal lending programs to more borrowers, with significant market scale as the FHA alone issued over 760,000 single-family home mortgages worth $230 billion in 2024. More favorable conditions were also created after Staff Accounting Bulletin No. 121 – the rule preventing banks from providing cryptocurrency-backed loans – was repealed when President Donald Trump took office.

However, integrating Bitcoin into the mortgage system also faces serious challenges, particularly the high volatility of cryptocurrency that could cause sharp BTC price drops, increasing loan-to-value ratios and triggering margin calls or forced liquidations.

Furthermore, traditional risk models assume relatively stable income and assets, while with cryptocurrency, net worth can fluctuate 50% in a week, creating significant challenges in risk assessment for financial institutions.

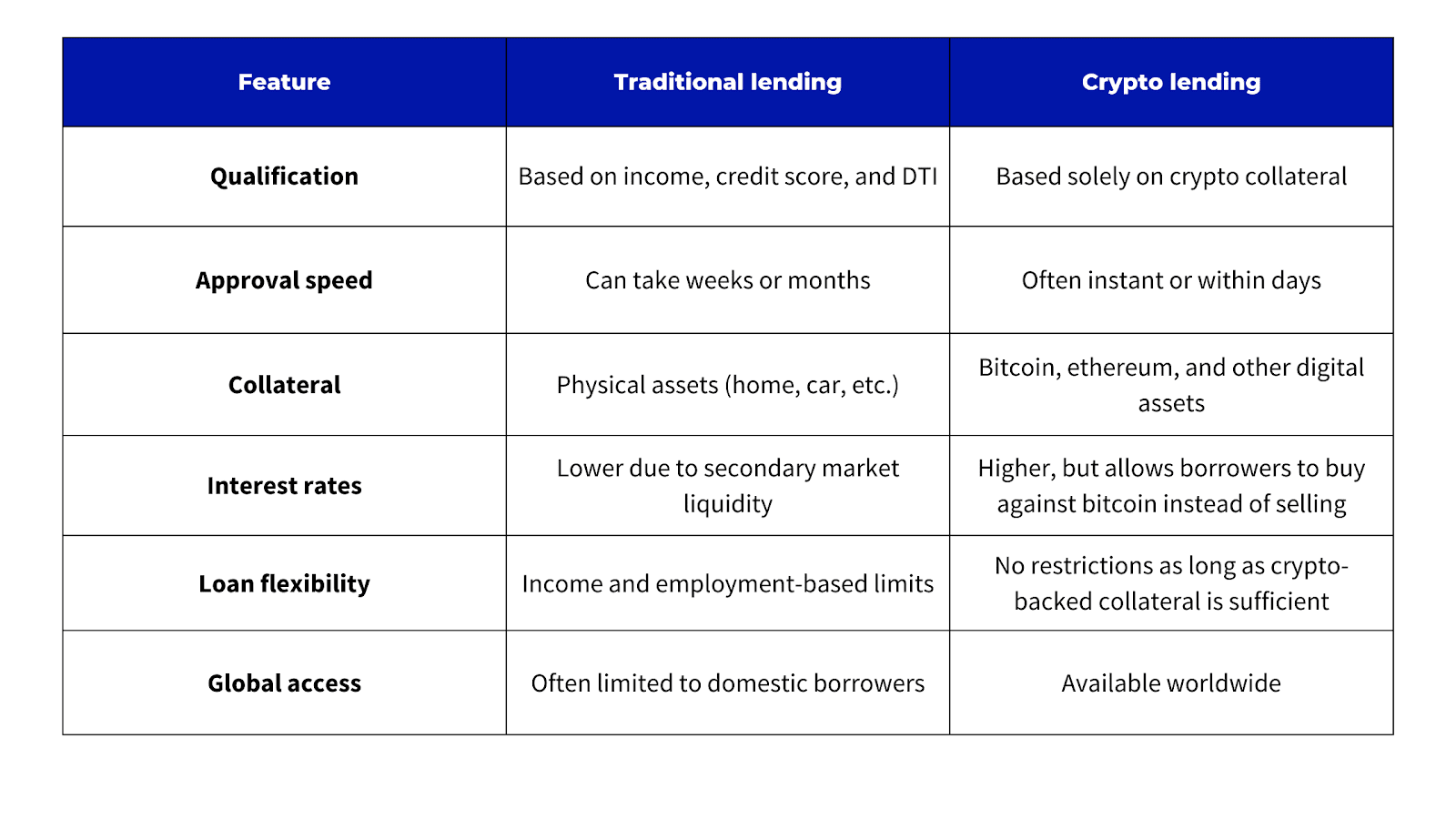

Current Cryptocurrency Lending Market

Currently, the cryptocurrency lending market is quite limited with only a few specialized lenders such as:

- Milo (formerly MiloCredit) – a company that approves loans instantly but requires borrowers to prove they have enough cryptocurrency to cover the entire loan value, primarily serving second home purchases, vacation properties, or investment properties

- Strike – a company providing Bitcoin-backed mortgage loans but warning about volatility risks and forced liquidation

These cryptocurrency loans primarily target a special customer group including high-income investors, real estate investment buyers, and those who don’t qualify for traditional bank loans due to complex income structures or assets primarily in cryptocurrency form.

Future of Bitcoin in Housing Mortgages

According to the “State of Cryptocurrency 2025” report by the National Cryptocurrency Association, an estimated 20% of Americans (65 million people) currently own cryptocurrency with 74% of cryptocurrency portfolios valued under $50,000, creating enormous market potential for Bitcoin applications in housing mortgages.

Bitcoin possesses unique advantages as collateral such as:

- Transparency with public transaction records on blockchain

- High liquidity allowing quick conversion to cash

- Convenient custody capabilities facilitating easy verification of ownership and value

Allowing cryptocurrency use as down payments or collateral could:

- Open homeownership opportunities for the growing number of cryptocurrency investors

- Help reduce pressure on the housing market amid the current crisis

- Create new financial models for the real estate industry

The FHFA’s consideration of accepting Bitcoin in housing mortgages marks an important turning point in integrating cryptocurrency into the traditional financial system. Although many challenges remain to be addressed, particularly volatility issues and risk assessment, this move could open new opportunities for millions of cryptocurrency holders in the United States to access the real estate market.