Portfolio Management: A Beginner’s Guide to Building and Optimizing Your Investments

What’s an Investment Portfolio?

Picture your investment portfolio as a basket filled with different financial goodies—stocks, bonds, maybe even some cryptocurrencies. Each item in this basket is a financial asset, carefully picked to help you achieve specific goals. Instead of betting everything on one stock or asset (like putting all your eggs in one basket), a smart portfolio spreads your money across various investments. This strategy, called Diversification, is the heart of solid investing.

Why diversify? Because it’s like having a safety net. Different assets behave differently when markets shift. For example, when stocks take a hit, bonds might stay steady or even climb in value. By mixing things up, you reduce the sting of one bad performer dragging down your entire portfolio.

Building a diversified portfolio means choosing assets that match your goals, how long you plan to invest, and how much risk you’re comfortable with. A beginner might start with stocks and cryptocurrencies for growth, bonds for stability, and maybe a touch of commodities like gold. More seasoned investors might toss in real estate or other alternatives to spice things up.

Mastering Strategic Portfolio Management

Strategic portfolio management blends creativity with a structured approach. It’s about charting a clear course, syncing your resources, and remaining flexible as conditions evolve. This process contains five essential steps, each building on the last to guide you toward success. Let’s explore each one in depth.

Step 1: Define Your Strategic Objectives

The foundation of effective portfolio management begins with a clear vision. Start by pinpointing your long-term goals—whether you aim to drive innovation, fuel business growth, minimize risks, or maximize financial returns. These objectives act as your north star, shaping every decision that follows.

- Why It Matters: Without defined goals, your portfolio risks becoming a scattered collection of investments rather than a cohesive strategy. For instance, a tech startup might prioritize innovation by focusing on R&D projects, while a retirement fund might emphasize risk control and steady returns.

- How to Do It: Gather your team or consult financial advisors to brainstorm. Ask questions like: What does success look like in five years? Are we building for growth or stability? Write down specific, measurable targets—e.g., “Increase revenue by 20%” or “Reduce portfolio volatility by 10%.”

- Example: A company launching a new product line might set a goal to allocate 30% of its budget to market research and development, ensuring alignment with its innovation focus.

Take time to refine these objectives, as they’ll guide your resource allocation and keep your portfolio on track.

Step 2: Align Investments and Capacity

Once your goals are set, the next step is ensuring your investments and organizational capacity work in harmony to bring your strategy to life. This means matching your financial resources, team skills, and operational capabilities to the priorities you’ve outlined.

- Why It Matters: Misalignment can lead to wasted effort or missed opportunities. For example, investing heavily in a tech project without the right IT expertise can stall progress.

- How to Do It: Assess your current assets—cash, staff, technology—and compare them to your objectives. If your goal is growth through new markets, ensure you have the budget for marketing and the personnel to handle expansion. Adjust by reallocating funds or upskilling your team as needed.

- Example: A small business aiming to enter e-commerce might shift funds from traditional advertising to website development and train staff in digital sales, aligning capacity with its strategic shift.

This step ensures your portfolio isn’t just a list of investments but a living plan backed by the right resources.

Step 3: Get Real-Time Visibility at Portfolio Level

With your strategy in motion, maintaining real-time visibility into your portfolio’s performance is crucial. This step involves tracking key metrics—returns, risks, and progress—allowing you to make quick, informed adjustments.

- Why It Matters: Markets shift fast, and delayed insights can cost you. Real-time data helps you spot trends, like a sudden drop in stock value, and respond before losses mount.

- How to Do It: Use portfolio management tools or software to monitor performance dashboards. Set up alerts for significant changes and review metrics like ROI or market trends weekly. Compare your portfolio’s progress against benchmarks like the S&P 500 or your initial goals.

- Example: An investor might use a platform to track a diversified portfolio and notice a 5% dip in cryptocurrency holdings. With real-time data, they can decide whether to hold, sell, or rebalance into bonds.

This visibility keeps you agile, ensuring your portfolio stays aligned with your strategic vision.

Step 4: Adopt Hybrid Methodologies

Not all projects or investments fit a single approach. Adopting hybrid methodologies means blending traditional planning (like long-term budgeting) with agile techniques (like iterative adjustments) to manage your portfolio effectively.

- Why It Matters: A one-size-fits-all method can stifle flexibility. For instance, a long-term bond investment benefits from steady planning, while a tech startup venture might need quick pivots based on user feedback.

- How to Do It: Combine structured timelines for stable assets with flexible sprints for innovative projects. Use project management frameworks like Scrum for agile components and Waterfall for fixed plans, tailoring your approach to each investment type.

- Example: A portfolio manager might use a traditional schedule to oversee bond maturities while applying agile sprints to adjust a crypto trading strategy based on market volatility.

This hybrid approach lets you handle diverse initiatives with the right balance of control and adaptability.

Step 5: Adaptive and Ongoing Management

Portfolio management isn’t a one-and-done task—it’s a continuous cycle of monitoring, learning, and adapting. This final step ensures your strategy evolves with changing markets, goals, or external factors.

- Why It Matters: Sticking to an outdated plan can lead to missed opportunities or unnecessary risks. Regular adaptation keeps your portfolio resilient.

- How to Do It: Schedule quarterly reviews to assess performance against objectives. Gather feedback from your team or financial advisors, and adjust allocations as needed—e.g., shifting from stocks to bonds if the market turns volatile. Stay informed about economic trends to anticipate shifts.

- Example: After a year of strong stock gains, an investor might rebalance by moving profits into safer assets like government bonds, adapting to a more conservative stance as retirement nears.

By treating management as an ongoing process, you build a portfolio that grows and adapts over time, securing long-term success.

Mastering strategic portfolio management is about more than just picking investments—it’s about crafting a dynamic, goal-driven process. By defining clear objectives, aligning resources, gaining real-time insights, blending methodologies, and adapting continuously, you create a portfolio that thrives in any environment. Start with these steps, and watch your financial strategy come to life!

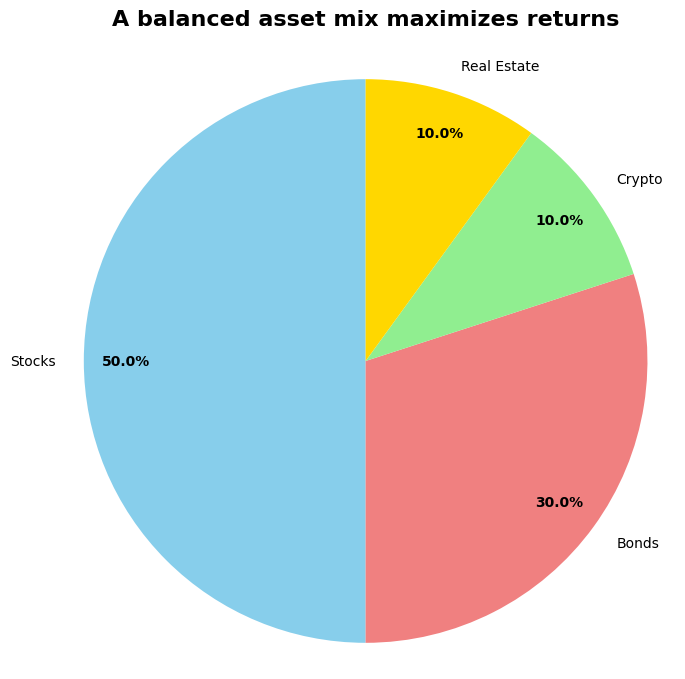

Boosting Returns with Asset Allocation

To get the most out of your portfolio, you need to allocate your assets wisely—think of it as mixing ingredients for the perfect recipe. The goal is to maximize gains while keeping risks at a level you can handle. Here are three common asset allocation strategies:

- Strategic Asset Allocation: This is a long-term plan where you set a target mix (e.g., 60% stocks, 40% bonds) based on your goals and risk tolerance. You stick to it and rebalance periodically to maintain that mix. It’s ideal for beginners or those with a long investment horizon, like a young investor eyeing retirement.

- Tactical Asset Allocation: This is more hands-on. You tweak your mix based on short-term market predictions. For instance, if you think cryptocurrencies are about to surge, you might temporarily boost your crypto holdings. It’s riskier but can pay off if your market calls are right.

- Dynamic Asset Allocation: This approach uses rules or algorithms to adjust your mix automatically based on market signals, like volatility or economic data. It’s complex and often best for experienced investors with access to advanced tools.

There’s no one-size-fits-all strategy. Your choice depends on your goals, how much time you can dedicate, and your market outlook. A solid allocation plan is key to growing your wealth while managing risks.

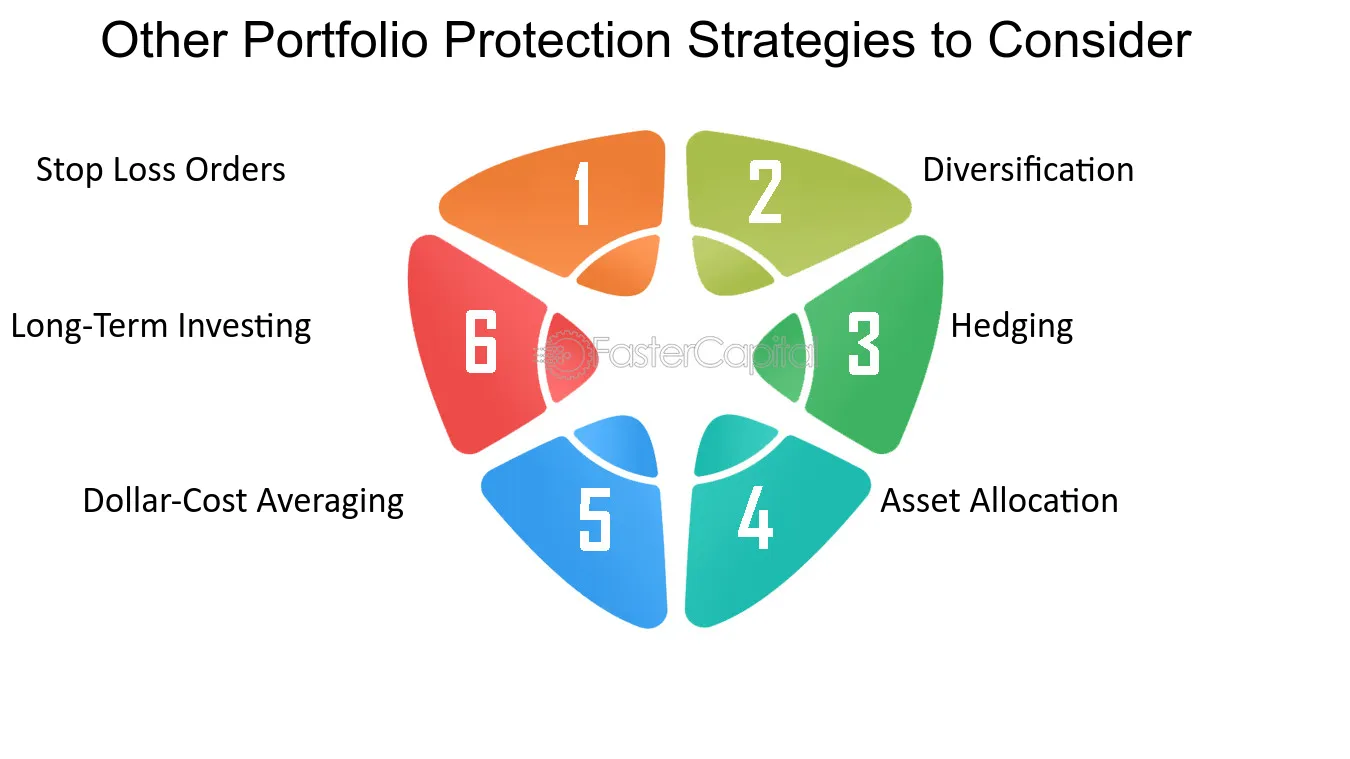

Controlling Risks: Protecting Your Portfolio

Investing always involves risk—it’s like crossing a busy street; you can’t avoid the cars, but you can look both ways. Risk control is about understanding and managing those dangers to protect your money and reach your goals. Here’s how to do it:

Assess the Risks

Your portfolio faces several risks, including:

- Market Risk: The chance that the whole market drops, affecting most investments.

Illustration Idea: A graph showing a stock market dip, with a red downward arrow labeled “Market Risk.” Place it here to show market fluctuations. - Credit Risk: The risk that a bond issuer (like a company) can’t repay its debt.

Illustration Idea: An image of a “default” stamp on a bond certificate, labeled “Credit Risk.” Place it here to highlight the concept. - Interest Rate Risk: When rising interest rates lower bond prices.

Illustration Idea: A seesaw with “interest rates” up and “bond prices” down, labeled “Interest Rate Risk.” Place it here to depict the relationship. - Inflation Risk: When rising prices erode your money’s purchasing power.

Illustration Idea: A dollar bill shrinking next to a grocery basket, labeled “Inflation Risk.” Place it here to show loss of value. - Liquidity Risk: The chance you can’t sell an asset quickly without losing value.

Illustration Idea: A “For Sale” sign on a locked safe, labeled “Liquidity Risk.” Place it here to illustrate difficulty selling.

Know Your Risk Tolerance

Are you a worrier who wants safety, or a thrill-seeker chasing big gains? Your risk tolerance determines your investment choices. Conservative investors lean toward stability, while aggressive ones embrace volatility for higher potential rewards.

Diversify to Spread Risk

As we’ve said, diversification is your first line of defense. By investing across different asset classes, industries, and regions, you lessen the impact of any single investment flopping.

Use Asset Allocation

Your asset mix itself is a risk management tool. A heavier bond allocation might lower risk, while more stocks or crypto could amp it up. Choose a mix that fits your comfort level.

Consider Hedging

For advanced investors, hedging uses tools like derivatives (e.g., options) to offset potential losses. It’s like buying insurance for your portfolio but can be tricky for beginners.

Set Stop-Loss Orders

For actively traded assets like stocks, a stop-loss order automatically sells if the price drops to a set level, capping your losses. It’s like setting a safety valve.

Effective risk control means taking calculated risks that match your goals while having safeguards in place to limit downsides. It’s about balance, not avoiding risk altogether.

Exploring Asset Classes for Diversification

Diversifying your portfolio means including a range of asset classes, each with distinct characteristics in terms of risk and return. Let’s break down the key options and take a deeper look at cryptocurrencies, which stand out for their potential to deliver exceptional profits when managed wisely.

- Stocks (Equities): These represent ownership in a company and offer strong growth potential, though they can be volatile. To manage that volatility, diversify by selecting stocks from various industries like tech or healthcare, and across regions such as the U.S. or emerging markets.

- Bonds: Essentially loans to governments or companies, bonds pay you interest over time. They’re generally safer than stocks, with government bonds being the least risky, while corporate bonds vary depending on the issuer’s credit quality.

- Investment Funds: Mutual funds and ETFs pool money from investors to buy a diversified set of assets. They’re perfect for beginners seeking instant diversification with minimal effort, as they’re professionally managed.

- Real Estate: This includes rental properties or Real Estate Investment Trusts (REITs). Real estate offers steady income through rent and potential growth in property value, and it often moves independently of the stock market, adding stability to your portfolio.

- Cryptocurrencies: Assets like Bitcoin and Ethereum offer high-risk, high-reward potential, often outpacing other assets with returns like Bitcoin’s 250% gain from $20,000 to $70,000 in a year, compared to 7-10% for stocks or 3-5% for bonds. Their low correlation with traditional assets makes them a diversification tool, and pairing them with stable assets like bonds can balance volatility while capturing growth. Start with a small allocation (e.g., 5-10%), research thoroughly, and only invest what you can afford to lose.

- Other Assets: Commodities like gold or oil, currencies, and derivatives can add variety to your portfolio. These are often more complex and better suited for experienced investors due to their unique risks and market dynamics.

Choosing the right mix of these asset classes depends on your financial goals, investment timeline, and comfort with risk. While stocks, bonds, and real estate provide a solid foundation, cryptocurrencies offer a unique opportunity for outsized gains if you play your cards right. Just remember to balance their potential with careful risk management to truly harness their power.

Conclusion: Mastering the Art of Portfolio Management

Portfolio Management is a crucial skill for anyone looking to build wealth and achieve their financial goals through investing. By understanding the basics of portfolio construction, asset allocation, risk management, and diversification, you can create a portfolio that is aligned with your objectives and risk tolerance. Remember that Portfolio Management is an ongoing journey. Regularly review and adjust your portfolio as needed to stay on track towards your financial success. It’s not about chasing quick riches, but about building a solid, diversified, and well-managed investment portfolio that works for you in the long run.