China's e-CNY Digital Currency: Understanding the World's Most Advanced CBDC

To truly understand e-CNY, we need to recognize that this is not just another digital currency, but one of the most advanced and influential Central Bank Digital Currency (CBDC) projects in the world. The Chinese government has invested heavily in developing and piloting e-CNY since 2019, creating a significant breakthrough in the digital payments landscape.

What is e-CNY and Why Does It Matter? /

e-CNY (Electronic Chinese Yuan) is the official digital version of China's renminbi currency. To grasp its importance, imagine the transition from handwritten letters to email - both serve the same communication purpose, but the digital method offers superior efficiency and application capabilities.

The foundation for e-CNY's development began in 2014 when the People's Bank of China (PBOC) established a specialized research group for digital fiat currency. Two years later, the Digital Currency Institute was founded, marking China's serious commitment to developing next-generation payment infrastructure.

The primary driving force behind e-CNY's creation stems from the practical needs of the digital economy. The PBOC recognized that the rapid development of the digital economy requires a retail payment system that is secure, comprehensive, and suitable for modern technological trends.

Implementation Process and Application Expansion /

Since late 2019, the e-CNY pilot program has been implemented with an increasingly expanding scope. As of 2023, e-CNY has been tested in at least 26 locations across 17 cities and important regions, including major economic centers like Beijing, Shanghai, Shenzhen, and Suzhou.

A notable aspect of the e-CNY deployment strategy is its integration with popular mobile payment platforms. Alipay and WeChat Pay - the two giants in China's digital payment sector - have integrated e-CNY into their systems. This creates a smart combination: users can continue using familiar applications while experiencing advanced digital currency technology.

China is also expanding e-CNY trials for cross-border transactions, with Hong Kong playing a key role. Plans to allow Hong Kong residents to top up their e-CNY wallets through local payment systems demonstrate the vision of a connected digital payment ecosystem. A practical example is PetroChina's crude oil transaction in October 2023 - the first time a major oil transaction was paid entirely with e-CNY.

One of the biggest concerns about central bank digital currencies is the issue of privacy and surveillance capabilities. The PBOC has designed e-CNY with a "two-tier" mechanism to balance necessary transparency with personal information protection.

In this system, the PBOC issues e-CNY to authorized operators (such as commercial banks), who then provide services to end users. This design resembles a multi-story building: the central bank at the top level only views overall information, while individual details are processed at lower levels.

Changchun Mu, head of the PBOC's Digital Currency Institute, explained that operators will collect necessary personal information, but the PBOC only processes inter-institutional transaction data without storing personal information. Only when suspicious transactions occur can authorized agencies request access to detailed data to serve anti-money laundering and counter-terrorism financing efforts.

Expanding Service to International Users /

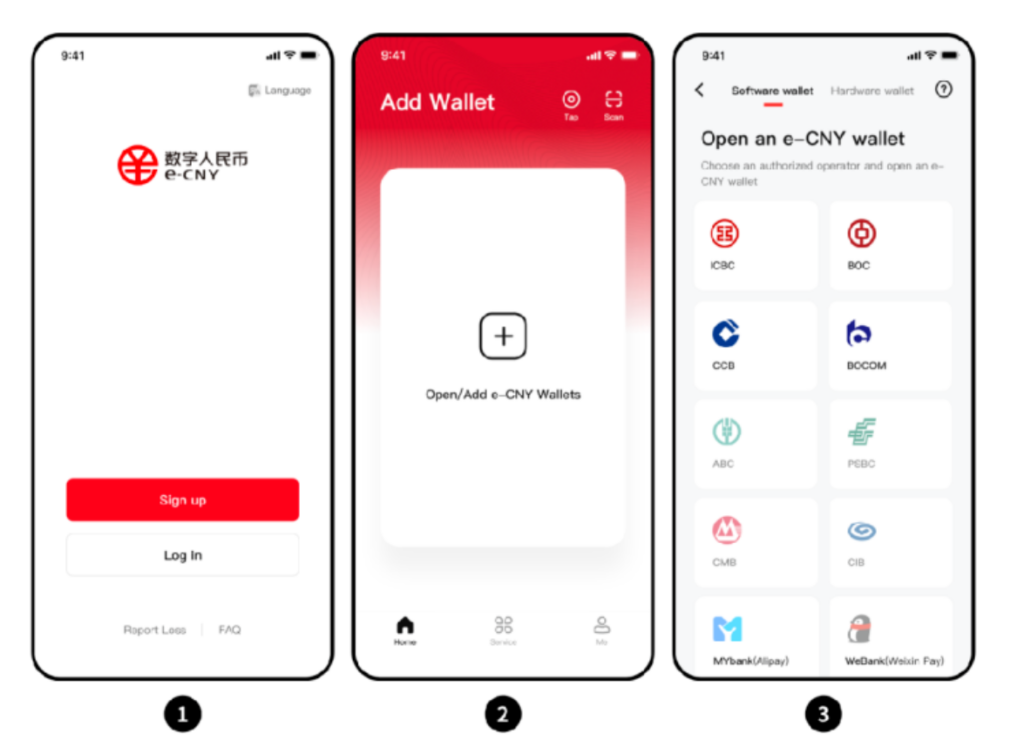

China is actively encouraging foreigners to use e-CNY when visiting and working in the country. In March 2024, authorities published detailed guidelines to help international visitors easily access and use e-CNY.

This process is designed to be very convenient: visitors can download the e-CNY pilot app and top up using their Visa or Mastercard. Notably, the system supports registration with phone numbers from over 210 countries and regions, demonstrating the global ambitions of this digital currency.

Significance and Future Outlook /e-CNY is not just a new payment tool but represents a completely different model for how currency operates in the digital age. The success of e-CNY is becoming a template for many other countries developing their own CBDCs.With its large-scale deployment, deep integration into existing payment ecosystems, and design that balances control with privacy, e-CNY is proving that central bank digital currencies are not only feasible but can bring real benefits to users and the economy. This is precisely why monitoring e-CNY's development becomes essential for anyone wanting to understand the future of the global financial system.

Understanding e-CNY helps us see how traditional monetary systems can evolve to meet digital age demands while maintaining the stability and trust that central bank-issued currencies provide. As we observe this groundbreaking experiment unfold, we gain valuable insights into how digital currencies might reshape global finance in the years to come.