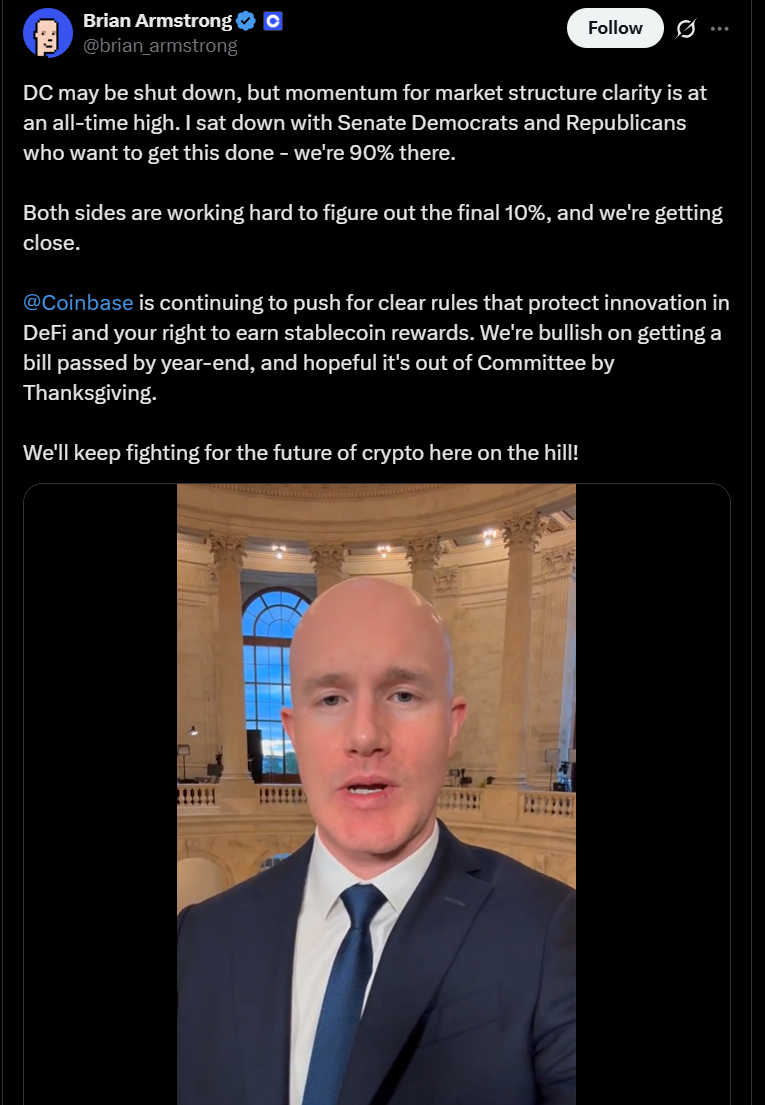

Coinbase CEO Says US Crypto Market Structure Bill is 90% Complete Despite Government Shutdown

- Coinbase CEO Brian Armstrong says the crypto bill is “90% done.”

- The final 10% focuses mainly on how to regulate decentralized finance (DeFi).

- Lawmakers aim to protect innovation while setting clear rules for centralized exchanges.

- Armstrong stresses the importance of preserving stablecoin rewards.

- Banks are lobbying against the GENIUS Act, fearing stablecoins could threaten their business model.

Coinbase CEO Brian Armstrong recently shared positive news about the progress of the US crypto market structure bill, even amid the ongoing government shutdown. Speaking in a video posted on X (formerly Twitter), Armstrong said that lawmakers are working hard to finalize the bill and could advance it by Thanksgiving.

According to Armstrong, around 90% of the legislative framework is already agreed upon. The remaining 10% of unresolved issues mainly concern decentralized finance (DeFi) – an area that requires careful regulation to avoid stifling innovation. Armstrong noted that lawmakers are taking a cautious approach, aiming to protect new technologies while ensuring centralized intermediaries like Coinbase are properly regulated.

He emphasized that DeFi protocols themselves should not be regulated in the same way as centralized entities. “Centralized intermediaries, like Coinbase, should be regulated – not the protocols,” Armstrong explained. This reflects a growing understanding among policymakers that the core value of blockchain innovation lies in decentralization and open access, not in creating more barriers.

Another key point Armstrong mentioned was the need to preserve stablecoin rewards. Earlier this year, the GENIUS Act was passed to set federal standards for stablecoin reserves, transparency, and consumer protection. Armstrong warned that large banks are now trying to roll back or block progress made under this act. “The big banks are coming for their cash grab, trying to block that. We’re not going to let them re-litigate that,” he said.

The banking industry has indeed pushed back strongly against the GENIUS Act. According to the Bank Policy Institute (BPI), the act creates a potential loophole that allows exchanges like Coinbase to offer interest indirectly to stablecoin holders. While the act bans stablecoin issuers from paying interest or yield directly, it doesn’t stop exchanges from finding ways to reward users — something that banks see as unfair competition.

This tension highlights a broader struggle between traditional financial institutions and the growing crypto economy. Many banks worry that stablecoins could threaten their business model, especially since traditional bank deposits offer little to no interest. As a result, stablecoins – which provide faster, cheaper, and more flexible digital payments – could attract users away from banks.

Industry experts, including Austin Campbell, a professor at New York University, have noted that banks are panicking over the idea of crypto users earning yields on stablecoins. The fear is that stablecoins could become a popular alternative to traditional savings, leading to a loss of deposits and market influence for banks.

Despite these challenges, Armstrong remains optimistic that bipartisan agreement is growing in Congress. Both political sides are beginning to see the importance of having a clear, fair, and innovation-friendly crypto framework in the United States. If the bill passes, it could provide much-needed clarity for the crypto industry, help attract more institutional investment, and strengthen the country’s position as a global crypto leader.

Final Thoughts

Even with the government shutdown and industry pushback, the US crypto market structure bill appears close to completion. Brian Armstrong’s optimism signals strong momentum toward a clear and balanced regulatory framework. Once finalized, this bill could become a major milestone for crypto in the US, paving the way for innovation, investor protection, and stronger market confidence.