Crypto Retirement Strategies: Why Older Investors Risk Everything

The Risky Gamble: When Traditional Retirement Plans Fail

Financial advisors have long preached the golden rule of retirement planning: reduce risk as you age. But what happens when your nest egg has already cracked? A growing number of older investors are defying conventional wisdom, turning to cryptocurrency as their last hope for a comfortable retirement.

Planning for retirement requires careful consideration – Source: Milvidskiy Law Group

The traditional 60/40 portfolio split between stocks and bonds no longer guarantees the retirement security previous generations enjoyed. With inflation eroding purchasing power and market volatility threatening savings, some investors aged 50 and above are making desperate bets on digital assets.

The Celsius Catastrophe: A Cautionary Tale

Alex P., a 52-year-old Sydney project manager, represents the extreme end of crypto retirement strategies. After losing 75% of his family’s savings in the Celsius collapse, he faced a stark choice: accept a reduced retirement lifestyle or double down on cryptocurrency investments.

“I completely drank the Kool-Aid of that business,” Alex revealed. The family had quit their jobs to live off Celsius yields, only to watch their dreams evaporate when the platform collapsed in 2022.

Crypto retirement dreams can turn into nightmares – Source: Cointelegraph

Despite the devastating loss, Alex has reinvested his remaining funds entirely in Bitcoin and other cryptocurrencies, including his Self-Managed Super Fund (SMSF). His strategy reflects a growing trend among older investors who feel traditional investment vehicles won’t bridge their retirement gap.

Professional Advice: The 25% Rule

Financial professionals strongly advise against all-in crypto strategies for retirement. Juanita Wrenn, managing director of Hudson Financial Partners, recommends capping cryptocurrency exposure at 25% of total retirement portfolio balance.

“That’s enough to benefit from upside if it performs, but not enough to cause catastrophic loss,” Wrenn explains.

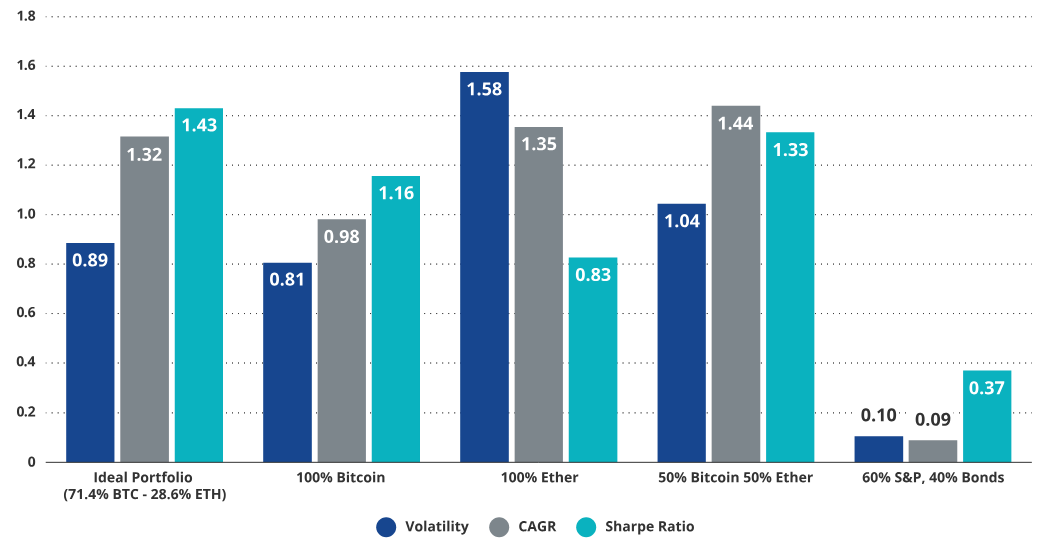

Optimal crypto allocation strategies – Source: VanEck

The reasoning is sound: cryptocurrency’s volatility can destroy retirement security overnight. A 50% overnight crash in crypto values could devastate an elderly investor’s financial future with no time to recover.

The Reality Check: Retirement Math

Most financial advisors recommend crypto allocations between 1-5% for retirement portfolios. This conservative approach allows investors to capture potential upside while protecting their core retirement funds.

For context, a modest Australian retirement account of $314,000 AUD ($205,000 USD) can provide comfortable retirement when combined with government age pension benefits. The key is preservation, not speculation.

Smart Crypto Retirement Strategies

1. The 5% Moonshot Approach

Allocate maximum 5% of retirement funds to cryptocurrency. This provides upside potential without risking catastrophic loss.

2. Dollar-Cost Averaging

Spread crypto purchases over time to reduce volatility impact. Many older investors find this approach more psychologically comfortable.

3. Bitcoin-First Strategy

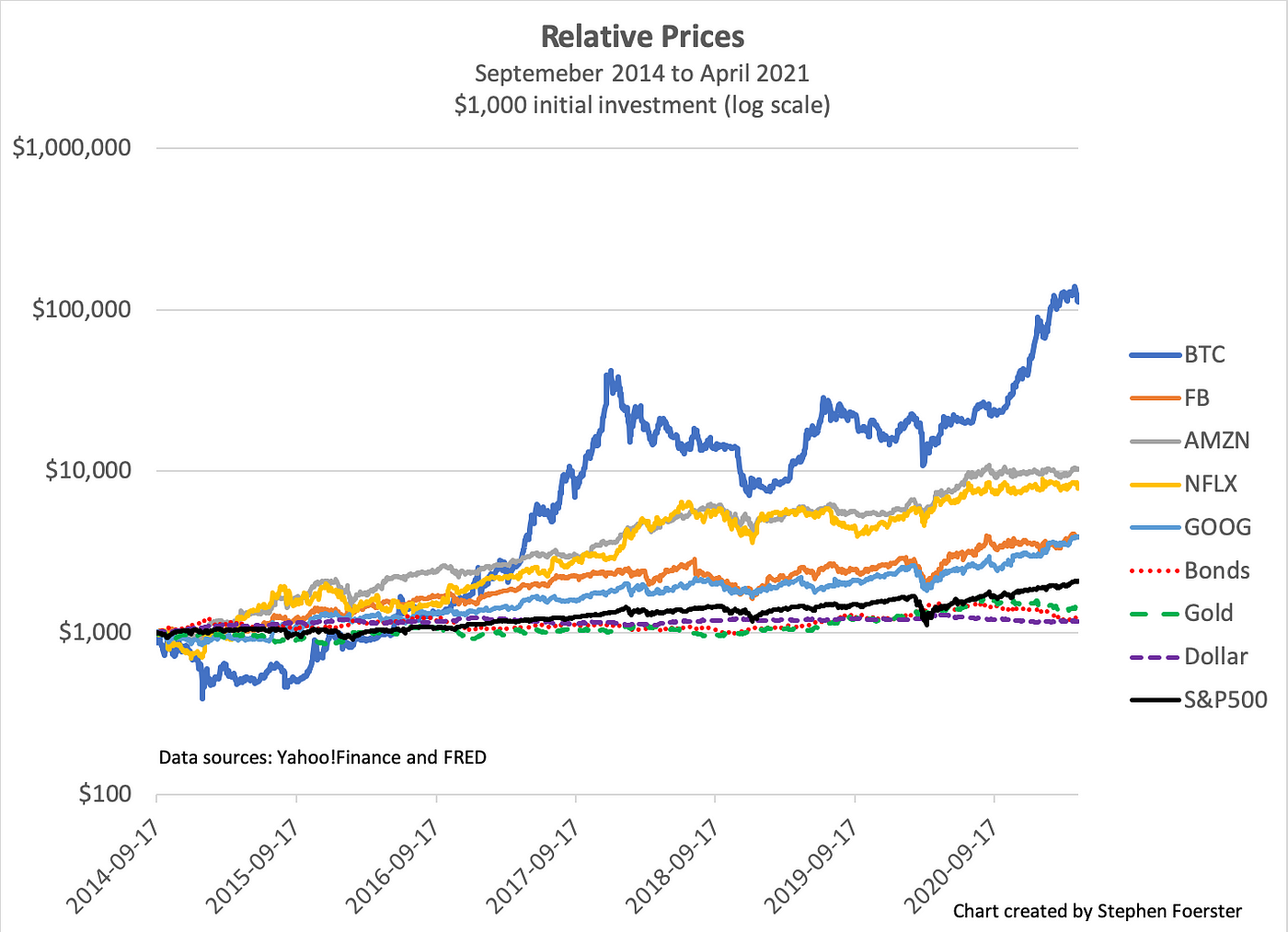

Focus on Bitcoin rather than altcoins. As the most established cryptocurrency, Bitcoin offers relative stability compared to newer digital assets.

Bitcoin’s risk-return profile over time – Source: Medium

4. Professional Guidance

Work with cryptocurrency-specialized financial advisors who understand both traditional retirement planning and digital asset risks.

The Regulatory Landscape

Cryptocurrency retirement options remain limited in most jurisdictions. In Australia, no superannuation funds currently offer direct crypto investment options, forcing interested investors into self-managed super funds (SMSFs).

The United States presents similar challenges, with employee-sponsored 401(k) plans generally excluding cryptocurrency options. However, recent regulatory changes suggest this may evolve, with the Department of Labor reversing previous guidance warning against crypto in retirement plans.

The Bottom Line: Calculated Risk vs. Desperation

“Crypto is volatility in a bottle — great if you sip, lethal if you chug,” warns US finance expert Eric Schiffer. His advice for older investors: treat cryptocurrency as a “5% moonshot sleeve” rather than a retirement salvation strategy.

The difference between calculated risk and desperate gambling often determines whether cryptocurrency enhances or destroys retirement security. While Alex P.’s all-in approach might pay off in a bull market, it could equally lead to financial ruin.

For older investors considering cryptocurrency in retirement planning, the message is clear: proceed with extreme caution, seek professional advice, and never risk more than you can afford to lose. Your golden years depend on it.