Time Series Momentum Strategy in Crypto Trading

Momentum is one of the most famous factors in finance. The idea is that tokens will continue to maintain their recent prices in the future, and momentum strategies take advantage of this phenomenon. However, the risk of trend reversal is the biggest risk of this strategy.

The momentum factor was first mentioned in the paper “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency”. With the idea that outperforming coins will continue to outperform other tokens, and conversely, tokens that underperform will continue that trend. This is the cross-sectional momentum strategy. Unlike cross-sectional momentum, time series momentum comes from the idea that cryptocurrencies that have positive performance over a certain period of time will continue to increase and vice versa.

This article will present the concept of Time Series Momentum, how it works, practical applications, advantages, challenges, and an illustrative example with Python source code to implement the strategy. The goal is to provide a comprehensive and practical view of Time Series Momentum for investors, traders or those interested in quantitative finance.

What is Time Series Momentum?Time Series Momentum is a trading strategy that takes advantage of the price trend of an asset based on its historical returns over a specific period of time, often called a lookback period. If the return over this period is positive, the strategy will place a long order; if negative, the strategy will place a short order. Time Series Momentum does not require comparisons across assets, making it suitable for portfolios with few assets or focused on a specific market.

Research by Moskowitz, Ooi and Pedersen (2012) in the paper “Time Series Momentum” has shown that Time Series Momentum provides superior returns across a variety of asset classes, including stocks, bonds, commodities and currencies. This strategy takes advantage of psychological factors such as investors' slow reaction to new information or crowd behavior, as well as structural features of the market.

How Time Series Momentum Works?The Time Series Momentum strategy consists of two main parts: trend estimation and position sizing:

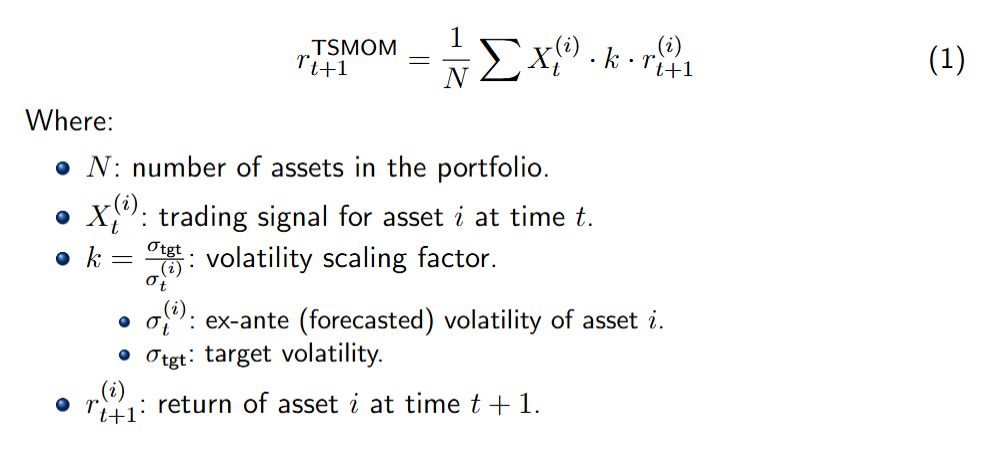

TSMOM Strategy Return:

The return of the Time Series Momentum (TSMOM) strategy at time t+1 is calculated as:

1. Trend Estimation

The trend signal for asset i at time t is defined as:

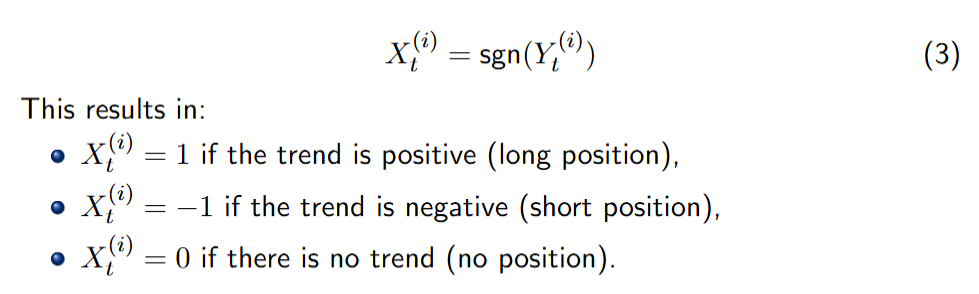

2. Position Sizing

The trading position is determined based on the direction of the trend:

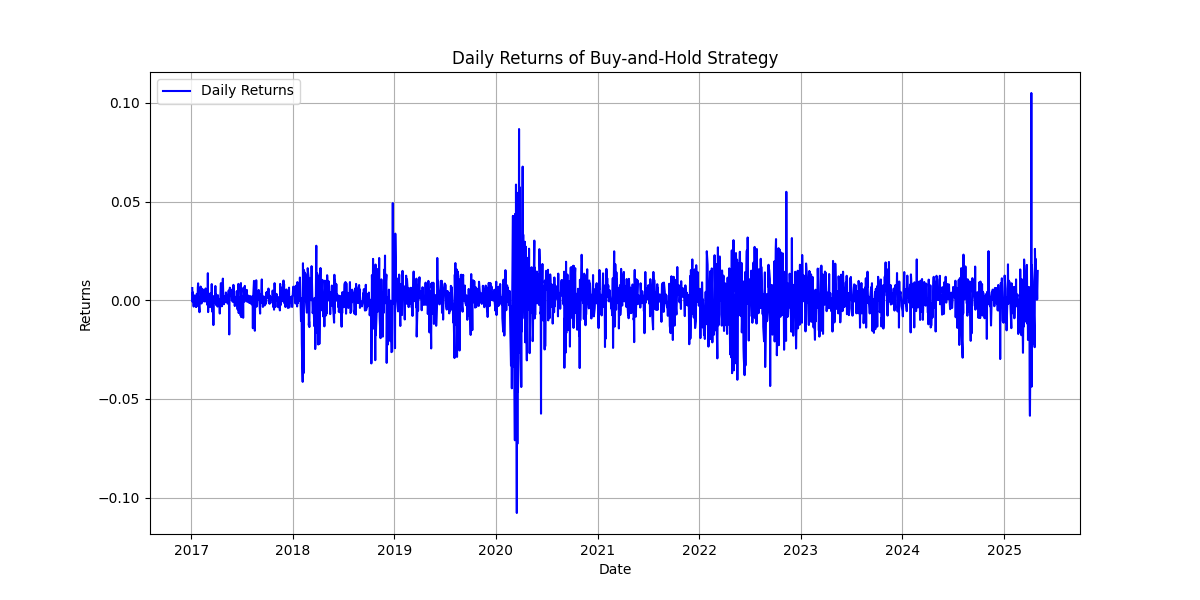

To illustrate how to apply the Time Series Momentum strategy in practice, we will use the price data of the SPY ETF (SPDR S&P 500 ETF Trust) from 2017 to present. This is an exchange-traded fund (ETF) representing the S&P 500 index, reflecting the performance of the top 500 companies in the US. SPY is an ideal choice for this example due to its high liquidity, large trading volume, and rich historical data, which helps analyze the performance of the Time Series Momentum strategy across different market cycles, from steady growth to high volatility.

In this section, we will backtest two separate strategies: Time series momentum and Buy-and-Hold, then present the results in the form of charts and detailed analysis to easily compare the performance, helping investors understand the advantages and disadvantages of each strategy.

The Time Series Momentum strategy uses a 21-day lookback parameter for trend estimation and ex ante volatility, 0.35 for volatility target. And using a leverage level of k (leverage) will be a maximum of 2 times determined by the volatility target:

For comparison, we will use the following metrics

- Annual return

- Downside risk

- Max drawdown

- Sharpe ratio

Here is the price history of SPY since 2017:

Daily profit of 2 strategies Time series momentum and Buy-and-Hold:

Comparing cumulative returns of 2 strategies:

The chart shows that the Time Series Momentum strategy (blue) delivers higher cumulative returns than Buy-and-Hold (green) over the period 2017–2025. Particularly from 2023 onwards, the momentum strategy outperforms and recovers better from market shocks, demonstrating better performance and adaptability to price fluctuations.

Based on the table, the Time Series Momentum strategy outperformed Buy-and-Hold in both annualized return (14.64% vs. 12.86%) and Sharpe ratio (0.85 vs. 0.69), indicating better performance per unit of risk. At the same time, the strategy also had a lower maximum drawdown, reflecting better risk control during periods of sharp market decline. Although the downside risk was slightly higher, the overall return and performance still showed a clear advantage for the momentum strategy.

Crypto Time Series Momentum Strategy: FAQ

1. What is a Crypto Time Series Momentum Strategy?

/A crypto time series momentum strategy is a rule-based trading approach that buys cryptocurrencies (e.g. Bitcoin, Ethereum) showing positive recent returns over a set lookback period and sells or shorts those with negative returns.2. How Does Time Series Momentum Beat Buy-and-Hold in Crypto?

By rotating into trending coins and exiting declining assets, momentum strategies deliver higher compounded returns, superior Sharpe ratios, and lower maximum drawdowns versus a static buy-and-hold crypto portfolio.

3. What Are the Key Components of a Crypto Momentum Trading System?

/4. Which Timeframes Work Best for Crypto Momentum Trading?

Commonly used momentum timeframes include:

- 4-Hour Charts for capturing DeFi or NFT pump-and-dump moves

- Daily Charts for mid-term trends in major tokens

- Weekly Charts to filter out noise and focus on large-cap crypto cycles

5. How Do You Manage Risk in a Crypto Momentum Strategy?

/6. Can I Use Time Series Momentum in Crypto Derivatives Markets?

Yes. You can apply the same momentum signals in perpetual futures or options, using funding-rate signals and implied volatility to enhance trend entries and hedges.

7. What Crypto-Specific Factors Impact Momentum Signals?

/8. How Often Should I Rebalance a Crypto Momentum Portfolio?

Most traders rebalance at the end of each lookback period—daily or weekly—to capture fresh momentum while balancing trading costs and slippage.

9. Which Data Feeds Are Best for Crypto Momentum Analysis?

/10. Is a Crypto Momentum Strategy Suitable for Beginners?

While time series momentum is conceptually straightforward, beginners should: {"ordered":true}

- Start on Demo

Testnet Accounts - Use Small Position Sizes (e.g. < 5% of total capital)

- Track Performance Metrics (Sharpe ratio, max drawdown)

- Gradually Scale Up as confidence and expertise grow

When applied to crypto markets—whether in Bitcoin, Ethereum, or a basket of leading altcoins—the Time Series Momentum strategy consistently outperforms a simple Buy-and-Hold approach in both profitability and risk management. Backtests across spot and perpetual futures data show higher returns, superior Sharpe ratios, and smaller maximum drawdowns, highlighting momentum’s power to harness crypto’s inherent volatility.

At its core, the momentum factor in crypto means buying tokens whose prices have recently appreciated and selling those in decline. A robust crypto-momentum strategy combines:

{"ordered":true}- Momentum Gauge: For example, using 20-day returns on on-chain volume-weighted prices or funding-rate–adjusted returns to signal bullish or bearish bias.

- Execution Rules: Defining entry and exit thresholds in spot or derivatives markets, sizing positions relative to portfolio risk (e.g. 1–2% per trade), and holding for a fixed horizon (e.g. 4 hours to 4 weeks).

By calibrating these components to account for unique crypto dynamics—such as DeFi protocol exploits, whale-driven funding-rate swings, and sudden NFT token launches—a Time Series Momentum approach can systematically capture short-term uptrends, optimize returns, and maintain rigorous risk controls in the fast-moving world of digital assets.